Case Study: Banca Monte dei Paschi di Siena

By: Nicola Bilotta

Between the beautiful hills of Tuscany stands Siena. Siena is a magical medieval city, which attracts tourists for its history and its monuments. But Siena hides many secrets. The destiny of the city has always been bound to Banca Monte dei Paschi di Siena (MPS) which is currently facing a significant crisis and is close to bankruptcy. The future of MPS is unclear, and plans for private recapitalization have failed. In December 2016, the Italian government approved a public fund of 20 billion euros to infuse capital inside the Italian banking system. If MPS does not raise enough private capital to increase its solidity, it will most likely be nationalized with the state as the main shareholder.

MPS is the sick man of European banking and its fragility is marked as a threat to the survival of the Italian banking system. Its attempts to increase its own capital are failing. The fall of MPS seems unavoidable. It is difficult to predict how and if the bank will be saved. But there is a lesson, which investors and banking regulators should learn from MPS’s story. The bank’s failure shows how lethal the detrimental bond between political power and banking activities can be.

This report explores the deep roots behind the MPS crisis, analysing how bad management ruined the oldest bank in the world. Administrative misbehaviour has two main roots. (1) MPS’s governance structure, which overemphasised the relationship between the bank and Siena’s territory. As management was the direct expression of political forces of Siena and Tuscany, business activities and plans were strongly influenced by external actors. (2) Bad management, a reflection of the corrupt system dominating MPS business, resulted in illegal financial operations which have destroyed the bank’s accounts.

There are additional causes and explanations to understand MPS’s failure. Several reports and comments give much attention to the roles of specific political parties, lobbies and private organizations. However, as these links are still not proved, I focus on the facts and numbers to show which factors are the main causes behind the MPS downfall.

Section I

1.1 The deep roots of the relationship between MPS and Siena

MPS has been lending money before Italy became one nation, before Martin Luther challenged the Pope and official Catholic doctrine and even before Shakespeare captivated the world with his plays. MPS’s long history started in 1472 when the Republic Magistrature founded Monte Pio, which provided loans to underprivileged people in the city with an interest of 7.5 percent. Monte Pio survived medieval economic and political crises that damaged the city of Siena. During the XVI century Monte Pio started to transform its activity, becoming an orthodox commercial bank and it even served as an institution with public functions.[1] Here, the tight relationship between MPS and the city of Siena began. In 1624 Siena received permission from the Duke to expand Monte Pio’s business and to create Monte non valicabile dei Paschi e della città e stato di Siena. In 1783, the two banks were reunited in one institution called Monti Riuniti changing its name to Monte dei Paschi di Siena in 1872.[2]

The bank contributed millions every year to the social, cultural and economic activities of Siena’s territory. In 2006 Siena was elected the Italian city with the highest quality of life. Such a great result was due to the fund of 197 million euros which Fondazione Monte dei Paschi allocated to modernize the city.[3] Until the crisis hit MPS hard, no one in Siena would have complained about the governance, as from 1966-2010 the management of the bank allocated around 2 billion to Siena and its province.[4]

For more than a decade MPS sponsored the Siena soccer team without any notable success. According to the expert Marotta, in the season of 2011/2012 MPS not only allocated around 8 million euros in sponsorship to the team – representing 15% of its annual revenues – but it also guaranteed more than 10 million euros of the team’s debts.[5] From 2000 MPS also become the first sponsor of the local basketball team that won eight consecutive Serie A (the highest domestic league in Italy) titles between 2006 and 2013. Bologni explains how 4/5 of the 21 million annual revenues in the season 2011/2012 was provided by MPS and its business relationships.[6] Even though in the history of Siena basketball and soccer teams had different athletic success, they shared a common destiny. When MPS had to drastically reduce its investments, both organizations were dramatically impacted as the bank cut all its sponsorship funds directed to them. Consequently, they declared bankruptcy.

1.2 The role of Fondazione Monte dei Paschi di Siena

1.2 The role of Fondazione Monte dei Paschi di Siena

Since the founding of MPS, the tight connection between the bank and Siena’s dynamics has never been interrupted. The commitment of MPS to the city of Siena is confirmed by MPS’s own statute: “Due to the historical and traditional relationship between the city and MPS, the council benefits a proportion of Fondazione del Monte dei Paschi di Siena’s profits. The council appoints half of Fondazione’s directors, who are people living in Siena or in its province.”[7] So the link between MPS and Siena is fortified by (1) the power of the council to appoint the management of the bank and (2) the benefits distributed from the bank to the territory of Siena.

As highlighted by the Tuscany Commission investigating MPS’s crisis, the link between MPS and the institutional framework of Siena can be summarized in three main points:

- Political control over Fondazione dei Monte dei Paschi di Siena(FMPS)

- FMPS ownership of 51% of MPS shares

- Funds allocated from MPS and FMPS to Siena’s territory

In 1995 MPS’s governance was completely transformed to meet requirements of a new banking law. The bank was transformed into a corporation called Banca Monte dei Paschi di Siena, which combined all financial, credit and insurance activities of the group. FMPS was founded as a non-profit entity with the function as major shareholder of the new corporation. Its statute states that “It has the purpose of contributing to charity and aid, in addition to giving social support in sectors such as scientific research, education, health and the arts, especially focused on the city and province of Siena.” Here, again, the link between the entity and the city is legally established.[8]

FMPS controlled MPS because it owned 51% of MPS shares until 2012 and 33% between 2012 and 2014. Therefore, who controlled the former, de facto governs the latter. In addition to this fact, until 2013 MPS’s statute said that no other shareholders could own more than 4% of the bank’s shares. Before the new statute of FMPS was approved in 2013, the 16 members of the Depatuzione Generale were nominated as listed:[9]

- 7 by the Council of Siena

- 1 by the Council of Siena in accordance with the Camera di Commercio, Industria, Artigianato e Agricoltura[10]

- 5 by the Province of Siena

- 1 by the Tuscany Region

- 1 by the University of Siena

- 1 by the dioceses of Siena-Colle Val d’Elsa-Montalcino

The Duputazione Generale is the main executive body of FMPS. It plans and formulates any business strategy of the institution. It used to command how MPS was governed, making FMPS an expression of Siena’s territory and its political power. As 14 out of 16 members were directly nominated by political institutions, there was a conflict of interest between administrative local councils and FMPS. As confirmed by Valentini, current Major of Siena, “Inside FMPS there was an intrinsic power of both local institutions governed by politicians for the majority and national political entities. There was a supply chain with local and national inputs[11]which strongly influenced FMPS’s decisions and MPS’ activities.

FMPS has two endogenous fragilities due to its close relationship with political institutions. (1) It does seek to maximize profits but it privileges distorted investments influenced by politics. (2) As FMPS does not have a source of cash flow but only uses credits produced by MPS, in case the bank needs to be recapitalized, FMPS would not be able to provide any further funds. To make sure it would not lose control of the bank’s governance, FMPS would not easily call for an external capitalization. As Boeri and Guiso note, FMPS preferred to increase its debts rather than reduce its shares in MPS. This irrational strategy clearly shows how FMPS aimed to remain in control of MPS even though it would have meant sacrificing the wellbeing of MPS.[12]

Section II

In order to understand the path to MPS’s failure, the analysis needs focus on bad management through two main tenets: (1) creative financial operations and (2) values of non-performing loans.

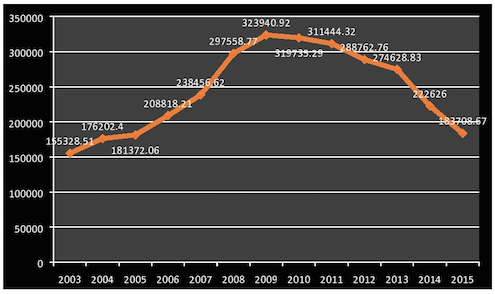

Graph 1: MPS Total Assets between 2003 and 2015 (‘000 Euros) (Bilotta)

2.1 Creative Accounting and Bad Business Instincts

In the period 1997-2007 the Italian political and economic authorities fostered mergers and acquisitions between banks. From 1995 MPS bought several Italian banks to expand its business and to improve its profitability. The horizontal integration was supposed to make MPS an international player in the financial system. In 1998-1999 MPS acquired the majority of Banca Agricola Montovana’s and Banca del Salento’s shares. The former operation was negatively valued by FITCHA-Ibca, which considered the acquisition of Banca Agricola Montovana a potential threat to MPS’ capital.[13] The acquisition revealed the corrosive bond between political interests and MPS. According to the Tuscany Commission, MPS acquired 52.94% of the bank for 1.600 billion Lira as a first step and the remaining shares for 900 billion lire later on. At that time Banca del Salento had 1,400 employees, 1,700 promoters and its financial sources were about 16,000 billion lire. Cenni[14]admitted to the Commission that MPS overpaid for Banca del Salento. The actual amount of money MPS paid for Banca del Salento was almost five times larger than Banca del Salento’s assets.

MPS completed its own destruction with the purchase of Banca Antonveneta. In 2007 Banca Antoveneta was acquired by Banco Santander from ABN Amro for 5.7 billion euros. Just a few months later MPS bought Banca Antonveneta for 9.25 billion euros from Banco Santander. In short, Banco Santander realized a capital gain of more than 3 billion euros in a few months. What could have explained an increase of 39% in Banca Antonveneta’s worth? According to the Italian Public Prosecutor and to Banca d’Italia records, MPS transferred more than 19 billion euros to ABN Amro, Banco Santander and Abbey National Treasury Service for the Banco Antonveneta because it also had to pay an additional 10 billion euros to cover Banco Antonveneta’s deficit. Italian prosecutors are still investigating which entity MPS paid to cover all Banca Antonveneta’s debts.

MPS did not just overpay for Banca Antonveneta, but there is evidence suggesting MPS management acquired the bank without due diligence on Banca Antonveneta’s accounts. As confirmed by the Commission, “For Santander it was crucial to sell in a short time in order to avoid Banca d’Italia’s checking of Banca Antonveneta’s accounts. At the time, It was looking for a buyer which was willing to accept the sine qua non condition of acquiring Banca Antonveneta without preventive due diligence. In other words, Banca Atonveneta’s purchase was made without a prior analysis of the bank’s accounts and, consequently, without knowing which was the right and fair value of bank’s assets.”[15] In poker parlance, for MPS it was a blind all in with a low two pair. Unfortunately, MPS was playing with its investors’ and savers’ money by investing about 19 billion euros in a weak bank.

In addition to the lack of research before acquiring Banca Antonveneta, there are doubts and mysteries on how MPS decided to finance the purchase of Banca Antonveneta. MPS management made a plan to pay Banco Santander by cash. 50 percent of the expense would have been covered by an increase in MPS capital, 20-25 percent by selling non-strategic assets and the remaining amount from available liquidity. As verified by Italian prosecutors, MPS used three illegal operations to raise funds to finance Banca Antonveneta’s acquisition. MPS management utilized creative financial manoeuvres to hide its exposure to risks.

- MPS created and sold JP Morgan a hybrid instrument called FRESH (Floating rate equity-linked subordinated hybrid preferred securities) to fund its re-capitalization for a value of 1 billion euros due in 2099. The function of FRESH bonds was to increase MPS capital without exposing FMPS to loss of its control over the bank as FRESH were more like bonds than a hybrid equity instrument. The aim of the operation was to allow MPS to raise its Tier 1 capital to demonstrate enough solidity to fund Banca Antonveneta’s acquisition. An additional 1.6 billion euros was raised through a subordinate bond called “Upper Tier 2” and it was strictly linked to MPS’s performance. Normally those kinds of bonds are sold to institutional investors who are aware of their high profile risk. Even though MPS said it had not sold this product to retail customers, 40,000 small investors had them in their portfolio.

FRESH will pay a quarterly coupon of 3-month EURIBOR plus 0.85%. The conversion price is EUR 4.179, representing a 25% premium to the reference price of EUR 3.3432. FRESH will automatically exchange into the underlying BMPS shares if, at any time, BMPS share price reaches 120% of the conversion price for 20 out of 30 consecutive days. BMPS and JPMorgan will enter into a derivative agreement, which, amongst other things, will allow BMPS to receive the annual dividends and a 25% “conversion premium” to the selling price of EUR 3.3432 at the time of the conversion of FRESH, in exchange for quarterly coupon payments on the FRESH of 3-month EURIBOR plus 0.85%.[16]

FMPS acquired FRESH for a value of 490 million euros, which were used to cover loans from Mediobanca’s and Credit Suisse’s. Due to the mechanism of FRESH bonds, “If that year (2008) MPS had closed with losses, FMPS would not have collected its coupon of 7 million and it would have paid interest to Mediobanca and Credit Suisse on its loans, of around 14 million euros ”.[17] MPS then had to close its year with profits otherwise it would have had to pay much more to its creditors.

Alexandria is the name of a derivate product MPS bought from Dresdner Bank in 2005 for the value of 400 million euros. At the time it seemed a good operation as Alexandria had an AAA rate and it was a synthetic CDO (Collateralized Debt Obligation). However, after Lehman Brothers’s fall, the value of derivatives worldwide dropped and Alexandria lost 30% of its initial value causing a debt of 220 million euros in MPS accounts. In order to cover its losses, in 2009 MPS concluded a secret agreement with Nomura whereby the latter had to acquire Alexandria’s products and MPS agreed to purchase 3 billion euros of 30 years BTPs (Italian Treasury Bonds) which “were then the object of an interest rate swap in which MPS was giving the fixed rate to the Japanese bank in exchange for a floating rate linked to the spread on Euribor.”[18] The aim of the operation was to allow MPS to close its fiscal year with significant profits and no losses.

- A similar agreement was signed between MPS and Deutsche Bank, the so-called Santorini investment. MPS decided to reduce its underlying volatility on its 3% Sanpaolo IMI equity stake. In 2002 MPS entered into an equity swap transaction with Deutsche Bank. In 2008 the value of Santorini investment recorded a loss of 367 million euros due to the financial crisis. In order to prevent recording its losses, MPS agreed to restructure the previous agreement with Deutsche Bank. The new arrangement set that MPS would acquire 1.5 billion euros of 30 year BTPs from Deutsche Bank and the cash to fund this operation was acquired by MPS through a repurchasing agreement on the same BTPs with Deutsche Bank. “The two banks then created an interest rate swap similar to the one of Alexandria. This way, losses were “shifted” from the equity swap to the BTPs. A loss on government bonds is more “appropriate” for a commercial bank like MPS than one on an opaque and complex financial instrument, with the additional upside that it would not appear on the Income Statement thanks to the repo agreement.”[19]As highlighted by Bloomberg, which could read the agreement: “The bankers did this by mixing in two interest rate triggers – that is, prices fed into a formula that would determine how much money the participants in the trade had to pay or receive from each other. However, this created a slight possibility that MPS could win both sides of the bet. To mitigate this potential Deutsche Bank loss –as much as 500 million – Deutsche Bank added a third trigger. Underlying the now complex flowcharts of rates, payments, and triggering events was the asset on which the transactions were to be based: about 2 billion euros in Italian government bonds.”[20]

MPS management played with numbers to manipulate its own accounts. The Italian magistrature is still investigating to find responsibility and identify guilty parties. It is clear that MPS management misbehaved in order to cover up its own mistakes. But burying your head in the sand is never the right answer.

2.2 Non-Performing loans

Corriere della Sera published a partial list of MPS debtors and, as non-performing loans have been the core issue of MPS vulnerability, it is interesting to see how MPS reached a bad ratio of non-performing loans. According to Gerevini, Antonio Muto, a famous real estate businessman in Italy, received 27 million euros to build hotels and cars parks in Mantova. 13 million euros were invested in the project while 14 million euros seem to have disappeared. Giuseppe Statuto, who owns the Four Seasons Hotel and the Mandarin Hotel in Milan has a debt of 160 million euros with MPS. Sorgenia Group had a debt of 600 million euros with MPS in 2014. The Mezzaroma family used up to 50 million euros of an MPS loan trying to acquire Siena Calcio a few years ago.[21] Instead, the Mercegaglia family had loans of more than 1.6 billion euros with MPS. A detailed analysis of MPS credits reveals that 70 percent of its insolvency is related to loans of more than 500,000 euros, 32.4 percent of them have received funds for more than 3 million euros. It is impressive to see how MPS key weakness is due to corporate loans.[22]

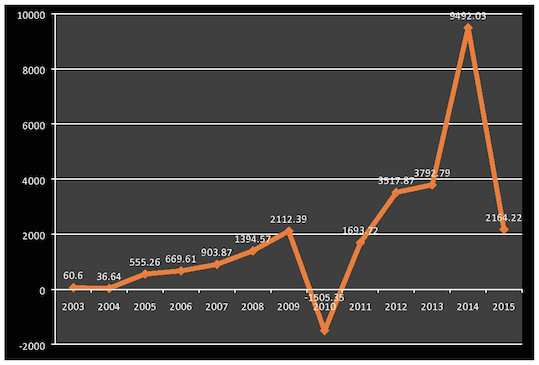

Italian prosecutors are trying to understand why MPS allocated loans to its clients. What needs to be clarified is whether MPS calculated and took into account risks in distributing its loans. Or, as it has been accused of, MPS management distributed loans neglecting any normal risk control in order to satisfy personal and political interests. To understand the bad NPL (non-performing loans) and impaired loans for MPS present and future, we need to take into account not just their values but also how much money the bank had to set aside for the provision of loans. If the former are sources the bank lost, the latter are sources the bank cannot use to invest in other projects. (See Graph 1 and Graph 2)

Graph 2: MPS Impaired Loans Provisions Values between 2003 and 2015 (‘000 Euros) (Bilotta)

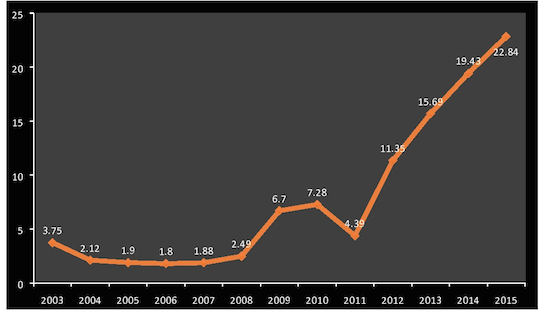

Graph 3: MPS Non-Performing Loans Percentage in Gross Total Loans between 2003 and 2015 (Bilotta)

As argued by Monti and Codogno,

A number of other factors have played a role in accounting for the high NPLs. A combination of over-indebted corporates following the sharp crisis-related drop in output, a highly complex legal system of corporate restructuring and insolvency, lengthy judicial processes, and a tax system that until recently discouraged NPL write-offs have all contributed to a rising stock of NPLs. While flows have become marginally negative, their stock remains among the highest as a percentage of total loans in the Euro Area, and the pace of write-offs has not increased significantly.[23]

Even though the crisis strongly impacted the Italian economy, there are no rational or business explanations that can potentially justify such an incredible level of NPLs. In other words, neither bad luck nor bad business instincts could have led to such a high NPLs.

Not a Good Idea: Politicians Controlling Banks

MPS is the story of a business and financial disaster. In only a few years its managers have destroyed the history and the assets of the oldest bank in the world. MPS is an interesting case study that demonstrates how mixing political interests and private banking is a fatal combination. (1) Its management is an expression of political games and, consequently, itd strategies are strongly influenced by external factors. (2) As a result, managers might promote business not looking for rational profits but for satisfying external requests. In conclusion, the context in which MPS operates is subject to non-market related dynamics that dominate business decisions.

MPS had total assets of 208.818 million USD and a Tier 1 of 8.625 million USD in 2006. Eleven years ago it figured at the 89th place of the Top 1000 World Banks by Tier 1 published by the Banker. MPS’s share value dropped from 102.29 euro in July 26th2006 to 15.08 euro when the shares were suspended from trading in December 23rd 2016. Now it is near to collapse trapped in investigative inquiries, huge debts and lack of capital. To understand how MPS reached this bad state, we need to take into account two main related causes: (1) MPS had a governance structure where its management was chosen by FMPS, a non-profit entity controlled by political institutions; (2) MPS management approved business plans influenced by external authorities, which eventually led to the bank’s disintegration. The trigger for MPS’s cascading vicissitudes was the acquisition of Banca Antonveneta generating collateral illegal operations (FRESH’s, Santorini Investment and Alexandria). MPS clearly shows how bad management and political interests can destroy a bank.

-x-

End Notes

[1] I Secoli del Monte. Cenni storici sulla Banca Monte dei Paschi di Siena e sui Palazzi della sua sede storica, P. 6-31

[2]D. Cristoferi, La ‘costruzione’ della Dogana dei Paschi di Siena in Maremma (1353-1419), 2015

[3]Ibidem

[4]http://www.reuters.com/article/italy-montepaschi-foundation-idUSL5E8GA76C20120510, 10/05/2012

[5]N. Cadirini, MPS: che fine farà il Siena senza la sua banca, Panorama, 6/2/2013 http://www.panorama.it/sport/fairplay/mps-che-fine-fara-il-siena-calcio-senza-la-sua-banca/

[6]M. Bolognini, Mens Sana dalle stelle alle stalle, La Repubblica Firenze, 05/02/2014

http://firenze.repubblica.it/cronaca/2014/02/25/news/mens_sana_dalle_stelle_alla_liquidazione-79555228/

[7]Fondazione Monte dei Paschi Statute, p. 23 “In virtù dello storico e tradizionale rapporto tra la città e il Monte dei Paschi di Siena, il Comune di Siena è beneficiario di parte degli utili della Fondazione del Monte dei Paschi di Siena, nomina la metà dei membri della Deputazione Generale della Fondazione, scelte fra persone domiciliate in Siena e/o nella sua Provincia; la potestà di nomina è attribuita al Sindaco sulla base degli indirizzi definiti dal Consiglio Comunale.”

[8]Fondazione Monte dei Paschi di Siena’sStatute, p.2

[9]Ibidem, p. 3

[10] Camera di commercio is a traditionalentitywhichassociateslocalentrepreneurships

[11]Report Commissione d’inchiesta Regione Toscana, p. 26Sulla Fondazione c’era un ruolo, allora ancora più importante, delle istituzioni locali governate dalla politica, sia quella locale che, in parte minore, da quella nazionale e quindi c’era una filiera decisionale che influiva in modo forte sulle attività della fondazione e della banca, che deriva da input locali e input nazionali

[12]T. Boeri and L. Guiso, Quell’abbraccio mortale fra Fondazione e Banche, La Voce 13/01/2014

[13] Report Commissione d’inchiesta Regione Toscana, p.29

[14] Maurizio Cenni worked in MPS before serving as Major of Siena from 2001 and 2011

[15] Report Commissione d’inchiesta Regione Toscana, p. 44 “E per il Santander “era importante vendere nel breve periodo senza dove necessariamente attendere il materiale passaggio della Banca italiana (Antonveneta ndr) da AbnAmro a Santander. Il tutto individuando un acquirente che “avrebbe dovuto accettare la condizione non negoziabile di rilevare Antonveneta senza alcuna “due diligencepreventiva” cioè senza poterne verificare lo stato di salute e la conseguente congruità del prezzo richiesto.”

[16]Press Release MPS, BMPS ANNOUNCES PRICING OF THE SALE OF SHARES TO JPMORGAN AND OF THE FRESH EXCHANGEABLE BOND, 23/09/2005

http://english.mps.it/media-and-news/press-releases/ComunicatiStampaAllegati/2005/9560A0F9-9E98-4CD7-BE5B-4E4C9ABF0DA0_13894_23settembre.pdf

[17]M. Lillo, MPS il regalo della fondazione di 20millioni a Mussari, il Fatto Quotidiano, 25/01/2013

”Se Mps quell’anno avesse chiuso in perdita, la Fondazione (dal Fresh 2008 ndr) non avrebbe incassato la cedola di circa 7 milioni di euro (più bassa dell’anno precedente per via della discesa dell’Euribor) e avrebbe pagato invece l’interesse alle due banche (Mediobanca e Credit Suissendr) sul prestito, per circa 14 milioni di euro.”

[18]Focus on Monte dei Paschi di Siena, http://www.bsic.it/focus-on-monte-dei-paschi-di-siena/

[19]Ibidem, http://www.bsic.it/focus-on-monte-dei-paschi-di-siena/

[20]V Silver and E. Martinuzzi, How Deutsche Bank made 367 million disappear, BloombergBusinessWeek, 19/01/2017

[21] http://www.corriere.it/economia/17_gennaio_10/ecco-chi-sono-debitori-monte-paschi-23ac5820-d775-11e6-94ea-40cbfa45096b.shtml

[22]M. Gerevini, Ecco chi sono i grandi debitori di MPS, Corriere della Sera 10/01/2017

[23] L Codogno and M. Monti, Watch Italy’s referendum for potential banking problems, LSE blogs 22/11/2016

Bibliography

Banca Monte deiPaschi di Siena Annual Reports (2005-2015)

Report Commissione d’inchiesta della Regione Toscana su MPS, “Commisione d’inchiesta in merito alla Fondazione Monte dei Paschi di Siena e alla Banca Monte dei Paschi di Siena. I rapporti con la regione Toscana.”

Fondazione Monte dei Paschi di Siena Statute 2013

I Secoli del Monte. Cenni storici sulla Banca Monte dei Paschi di Siena e sui Palazzi della sua sede storica

- Boeri and L. Guiso, Quell’abbraccio mortale fra Fondazione e Banche, La Voce 13/01/2014

- Bolognini, Mens Sana dalle stelle alle stalle, La Repubblica Firenze, 05/02/2014

- Cadirini, MPS: che fine farà il Siena senza la sua banca, Panorama, 6/2/2013

L Codogno and M. Monti, Watch Italy’s referendum for potential banking problems, LSE blogs 22/11/2016

- Cristoferi, La ‘costruzione’ della Dogana dei Paschi di Siena in Maremma (1353-1419), 2015

- Gerevini, Ecco chi sono i grandi debitori di MPS, Corriere della Sera 10/01/2017

- Lillo, MPS il regalo della fondazione di 20millioni a Mussari, il Fatto Quotidiano, 25/01/2013

V Silver and E. Martinuzzi, How Deutsche Bank made 367 million disappear, BloombergBusinessWeek, 19/01/2017

Focus on Monte dei Paschi di Siena, http://www.bsic.it/focus-on-monte-dei-paschi-di-siena/

Monte deiPaschi, a legacy of power and history, http://www.reuters.com/article/italy-montepaschi-foundation-idUSL5E8GA76C20120510, 10/05/2012

Press Release MPS, BMPS ANNOUNCES PRICING OF THE SALE OF SHARES TO JPMORGAN AND OF THE FRESH EXCHANGEABLE BOND, 23/09/2005

Photo Courtesy of erasmusu.com